![]()

This publication considers the role of the downstream sector in meeting the UK's net zero target.

Download the report

The UK downstream oil sector is capable and willing to play a significant role in meeting societal targets for decarbonisation to net zero.

The Report makes three main findings:

Low-carbon liquid fuels can play a key role in the UK’s decarbonisation - and are doing so already. There are a number of technological pathways for the downstream sector to deliver further decarbonisation of products and their manufacture.

We see Hydrogen as a critical component of meeting net zero – the downstream sector is the largest producer of hydrogen in the world and can maintain and grow its role in producing and delivering zero-carbon emitting hydrogen.

A systems-based approach and enabling policy framework is required to produce low carbon- and eventually net zero liquid fuels. As part of this, consider bespoke approaches for sectors with limited decarbonisation options (aviation) to enable greater collaboration in supply chains’ pathways.

Pathway

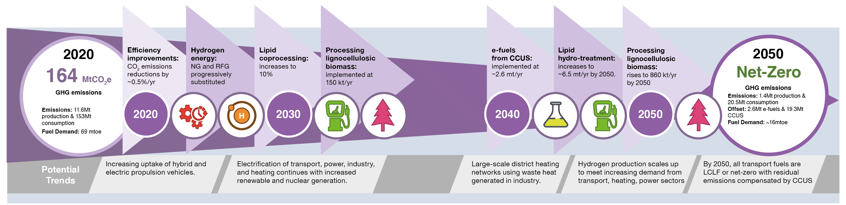

This pathway shows just one way that a net zero sector can be delivered – reducing manufacturing emissions from 11.6 Million Tonnes of Carbon Dioxide equivalent (MTCO2e) to 1.4 MTCO2e and potentially negative depending on use of CCUS, hydrogen and low carbon feedstocks for energy. As well as manufacturing this pathway shows that across the lifecycle of the fuels themselves can also be net zero – reducing the UK’s transport emissions by up to 153 MtCO2e.

Public Policy Recommendations

Today’s policies won’t be enough to deliver net zero as they don’t offer a reward for decarbonising at scale.

Fuels Industry UK believes that the following measures, if taken now, can deliver the necessary incentives to business to move to net zero while delivering a just transition

- Stimulate demand for LCLF's and hydrogen for transport;

- Ensure consumers are informed on the role of LCLFs for decarbonisation;

- Revise CO2 standards and emissions labels for vehicles to show lifecycle emissions;

- Industries and UK Government to develop sector-specific plans to decarbonise sectors with limited decarbonisation options (e.g. aviation);

- Clarify the expected role for hydrogen production and use in a comprehensive hydrogen strategy;

- Improve the UK industry’s competitiveness globally to secure the UK as first choice for decarbonisation investment

- Continue to promote industrial clusters with the downstream oil sector at their centre;

- Prepare the workforce to deliver net zero in a just transition;

- Ensure Government support for UK research, development and deployment of all manufacturing and transport decarbonisation technologies aligns with company needs; and

- Deliver a regulatory framework that allows for innovation.